|

Chasing debts is rarely an enjoyable activity when running a business, and you can be forgiven for not jumping on every overdue invoice the moment your payment terms have expired.

If an approach of just tolerating late payments sounds familiar, you're not alone. The Department for Business, Energy & Industrial Strategy found that over half of small businesses wait one month or more beyond their agreed terms for an invoice to be paid. With a fifth of SMEs waiting longer than two months! But when weeks turn into months which then turn into years, you may worry that you've missed your opportunity to take formal action. However, you may be surprised how long you have to pursue a debt before it is legally 'statute barred'.

Statute Barred Debts.

Being 'statute barred' means that the defined time period you have to use certain legal avenues to pursue a debt has expired. While this doesn't mean that the money is no longer due, or the debt no longer exists, it does restrict your legal options when pursuing a debt. So can be thought of as a legal time limit for invoices and other debts.

The time limits that formal court action must be made in the UK are detailed in the Limitation Act 1980 and court action is usually defined as a debt claim being issued at the county court or money claim online system. There are different time limits for different areas of law, but when the relevant time limit has passed, this act is able to be used as a defence by the debtor to prevent you obtaining a county court judgment (CCJ) against them. How long do you have to claim unpaid invoices?

Most invoices and debts fall under the definition of a 'Simple Contract' in the Limitation Act, meaning you have six years to commence legal action to recover the debt in England and Wales.

If money is owed in relation to a deed (i.e. a mortgage or property) then the limitation period is 12 years. You will also need to consider any pre-action steps that have to be taken before you issue proceedings such as the Pre-action Protocol for Debt Claims that may require you giving up to 30 days' notice before starting court proceedings. Once you have been through the court process and successfully obtained a court judgment (CCJ) against the debtor. You will generally then have a further six years from the date of the judgment to enforce it. When does the limitation period start for a debt claim?

For simple contracts the Act states that the limitation period will expire six years after the 'cause of action'. A 'cause of action' can be thought of as when a breach of your agreement has occurred.

For example, this could be when:

How to claim unpaid invoices.

Dealing with a debt that was incurred several years ago may seem like a complex process, but if you have documentary evidence that the amount is due it should not prevent you from pursuing the money owed to your business.

A solicitor will be able to advise you on your legal options to recover a business debt, including sending a letter before action, issuing a claim and potential limitation defences. Also if the debt isn't disputed you may be able to claim late payment interest and compensation which can be significant on long overdue debts. While six years may seem a long time, the sooner you act the more chance you have of recovering the amount owed and avoiding your debt claim being statute barred.

Comments

When you are owed money, hindsight can be a wonderful thing.

All too often in the rush to complete a business transaction or lending money to a friend in need, you won't think to put in place a legally binding agreement that formalises the arrangement beforehand. After all, you have every intention of holding up your end of the deal and so assume the other party will too. But if payment doesn't happen and your previous agreement starts turning into a dispute over what is owed, you may need to consider what legal avenues are open to you to get your money back. The success of any legal action will then depend on what evidence you can provide to show that the debt is owed.

Can you take someone to court for owing you money?

Yes, but the 'burden of proof' will be on you as the Claimant to show that the amount you are claiming is due. Court should be your last resort in attempting to recover your money and so you should be confident that you have a strong case, sufficient evidence and follow the set pre-action procedure prior to issuing a claim (e.g. sending a letter before action, attempting negotiation etc.)

Ultimately the decision on who owes what will be down to a judge's ruling based on:

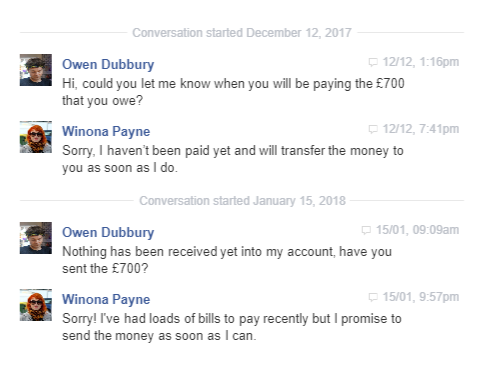

Owed money but no contract! SMS or messages on social media can help prove a debt is owed. SMS or messages on social media can help prove a debt is owed.

In the absence of a written contract or agreement being in place, there are various other pieces of information that you may be able to secure which can provide evidence that the money is due.

Bounced cheque or returned direct debit While the use of cheques is diminishing, hundreds of millions of cheques are still issued every year. If your debtor has sent you a cheque that bounced or agreed to a direct debit that has been returned, it is often all the evidence that you need to prove a debt is owed. In law a cheque is considered a 'promise to pay' and so can be used as a clear admission that money is due. Unpaid invoices It is not uncommon for a business to invoice without a contract. Most businesses use invoices to request payment so providing copies and proof of them being issued to a customer or supplier will go a long way in proving that a debt is owed, even if they aren't directly attached to Terms of Business or a contract. Furthermore, if you provided regular statements of the amounts owed and showing overdue, then these will also be useful as evidence. Evidence of chasing debts Once a payment is overdue you will have hopefully contacted the person or company to chase the debt. Emails, letters, texts or messages exchanged on social media (Facebook, Twitter etc.) can all be used to help prove a debt is owed and overdue. If the other party has responded to you apologising or asking for more time, then this admission will be extremely valuable in proving that they don't dispute that they actually owe the debt. So, it's important that you save or screenshot these messages in the event they are needed. Loaned money without a contract Without an I.O.U. or a loan agreement in place, proving that money provided to someone was a loan that needs to be repaid can be difficult. This is because often money given to friends, an ex, or family member is considered a gift and so isn't required to be paid back. Enforcing a verbal agreement that money is owed will hinge around providing evidence to show that the cash was transferred as a loan along with any repayments e.g.

Witnesses to the arrangement When little or no documentation exists to prove a debt, having an independent witness to a verbal contract can be invaluable. For example - with a business transaction, did an employee take the order over the phone, deliver goods or perform a service where payment was verbally agreed with the customer? If money was lent to a friend, was another person present to witness the agreement of how/when they were going to pay you back? But even if an independent witness isn't available, you as a claimant can also present your version of events to the court in a written witness statement. Any witnesses may then need to attend court should the claim go all the way to a hearing. Debt disputes with no contract.

Without a written agreement, there should still be plenty of information that you can pull together to prove what you are owed. However, if the other party disputes the amount, or that any debt is owed at all, then you may have a fight on your hands that needs to be settled in court.

It will then be down to the evidence you can gather and how your claim is pleaded to convince a judge that you are entitled to the money owed in the absence of a legally binding written contract. So, obtaining legal advice on the evidence needed for a debt recovery claim and your prospects should be your starting point.

When a friend asks to borrow money it can be difficult to refuse. We don't think twice about saying no or hanging up to telemarketers that want us to part with our money, however when it's someone familiar that is asking, your usual good judgement can quickly disappear.

But if after you have given the loan, your trusted friend disappears just as quickly, then you've now got a dilemma. This scenario is unfortunately all too common, with payment service Paym finding that over 12 million people in the UK admit to having fallen out with friends or family over money. Just under a third of these instances were from lending money to friends of only up to £100. But after repeatedly asking your friend for the money back, being reasonable and understanding of their circumstances but ultimately being left out of pocket, how can you get money back from someone who borrowed it? Can you actually take your friend to court? How can you prove you are owed the money?

Before involving the court you need to think about your prospects of success. You'll need to have some kind of evidence that you lent the money in the first place and that your friend hasn't paid you back.

If you've got a signed contract, loan agreement or IOU then that's ideal, but the evidence of the loan doesn't always necessarily have to be written. A legal contract can be verbal if it was just an arrangement you discussed and agreed between yourselves, however there still needs to be something that a court can see, like:

Does your friend actually have the money to repay you?

You can't get blood from a stone, so if your friend has no cash or assets then there may be little gained from taking them to court. It will cost you money to issue the claim and you'll rack up further fees to enforce any judgment from the court (bailiffs etc.) to perhaps end up with nothing or very little.

But if your friend is employed, owns a car, has equity in a house or some other assets that would cover the debt then it's reasonable to assume that you can make a recovery from them by going through the courts and obtaining a County Court Judgment (CCJ) against them.

How to get money back from a friend."Nearly 2 out of 5 people admit they don't always pay friends back, and one in ten say they have avoided paying money back to family on purpose." - Research by Paym  Not getting paid back can be frustrating Not getting paid back can be frustrating

If you've secured evidence of you making the loan and believe your friend has the means to pay you back, then it's time to start getting serious. Sometimes the realisation that you're willing to take the matter further can snap your friend into action.

First step is to write a simple (but formal) 'Letter Before Action' which gives your friend a final chance to settle the debt before court proceedings are started. As a minimum your letter should include:

Keep a copy for yourself and send the letter in the post to their home address, or where they are currently living. The best outcome is that your friend pays you back or at the very least you agree a payment plan that starts to recoup the loan. That way you avoid court costs and will eventually get your money back. If your friend subsequently fails to comply with the payment plan then at least you'll have further evidence to help with court proceedings. Also if you want to add additional weight to your claim, you can get a solicitor to draft and send the debt letter which should only cost around £50.00. Taking friends or family to the Small Claims Court.

The last resort in recovering your money is to take your friend to court. This is normally done through the small claims court (for amounts up to £10,000) and will involve you completing some paperwork, submitting it to the court and paying a court fee.

Instructions on how to make a claim can be found on the Gov.uk website. Straightforward claims are able to be done on your own with a little time and effort, but can get complicated if the claim is defended, interest is able to be added or bailiffs need to be instructed etc. As such depending on the amount, it may be wise to instruct a solicitor to handle the claim who should be able to do this for a fixed fee plus disbursements (the court fees). Some of your legal costs can also be recovered from the debtor as part of your claim. Remember getting money back from a friend, an ex-partner or family member can be complex and emotional process, so having your lawyer deal with the proceedings and ongoing contact with the debtor may help in the long run. "Before borrowing money from a friend, decide which you need most"

Being owed money by a trusted friend who won't pay you back is never a good situation to be in, and how you proceed will likely be determined by how much you want to maintain the friendship.

If your friend is in real financial difficulty then piling on court proceedings may not help them or their family, so you may want to consider the full impact of taking matters further. But this is a judgement and a financial call that only you can make. It is also worth noting that you generally have six years to start legal proceedings to recover a debt. You should never feel guilty about pursuing money owed to you which you lent in good faith. Remember if anyone has jeopardised your friendship it's a friend who has decided to stop paying and communicating with you. |

About UsCatalyst Law are team of legal professionals with over 20 years' experience helping businesses and people with their legal problems. Categories

All

Follow us on:Archives

March 2024

|

RSS Feed

RSS Feed