|

Thanks to a bombardment of TV, radio and online advertising over the last few years, the general public are now well aware of their rights to claim compensation if they've been injured and believe that someone else is to blame.

If these claims are made against you, either by a member of the public, a customer or an employee, it can be a daunting prospect thinking about how to defend the allegations. Especially when you believe that the person's injury claim has little or no merit. However there can be partial or full defences levelled against most personal injury (PI) claims. So it can be helpful to have a general awareness of the possible areas a solicitor may explore to defend the case against you to mitigate the costs of compensation. Admitting or denying liability in an injury claim.

Firstly, when an injured person (the claimant) makes a compensation claim against a business or individual (the defendant) the question of liability must be considered. Liability is whether the defendant was legally responsible for the incident and the resulting injury, and can also be thought of as being at fault.

When a claim is made, a defendant can either:

If a defendant admits full liability, then the claim will come down to the amount of compensation the claimant is entitled to. This amount can still be disputed (i.e. claimant's expenses are not justified) or negotiated (early out of court settlement) to minimise the cost. If the defendant denies liability or only admits being partially at fault, then a defence to the claim must be entered and there are several broad areas of defence that a solicitor can explore.

How to dispute a personal injury claim.

For the claimant to make a successful compensation claim they must prove:

The defendant had a legal duty of care towards the claimant and The defendant acted negligently so was responsible for the accident or incident and The claimant's sustained injuries were caused by the accident or incident As a defendant you may dispute any of these facts, ranging from how the accident occurred to proving that the injuries and financial losses were not a direct result of the accident. For example in cases such as a fall on business premises, a defendant may be able to produce CCTV or maintenance records to evidence that there were no hazards in the area and as such were not negligent in their actions. A company's health and safety policies, procedures and training are often relied on heavily when defending a claim that has occurred at a public place or place of work. So ensuring these records are documented and up to date can be a key evidence in a defence. Defence against personal injury claim.

No duty of care exists

Employers must ensure employees can conduct their work safely. Likewise the occupier of a building must ensure their environment is hazard free for customers or visitors. However not every relationship between two parties entitles one to a duty of care over the other. For example, while an employer may owe their employees a duty of care whilst working, the same may not be true for two self-employed contractors. Alleging fraud In extreme cases the defendant may dispute the fact that the accident even occurred at all and allege that the claimant is acting fraudulently. If evidence supports this allegation then not only can a case be dismissed, but the claimant may find themselves prosecuted and found 'fundamentally dishonest' forcing them to pay a defendant's legal costs. Alternatively, it may be accepted that there was an injury which was caused by the accident however the defendant may be able to obtain expert evidence to show the claimant is exaggerating their symptoms and losses. Contributory negligence While not a complete defence, contributory negligence is where the injured person is in some way at fault for the accident or incident which caused their injuries. So, while the defendant was partially to blame, so was the claimant. For example, in road accident claims contributory negligence is often applied in cases where the injured person wasn't wearing a seatbelt. While the defendant may have caused the accident by colliding with the claimant, the injuries the claimant sustained were also partially due to their own negligence in not wearing a seatbelt. As such if the claimant was awarded £4,000 for their injuries but found to have been 25% to blame for contributing to them, only £3,000 would need to be paid by the defendant. If contributory negligence can be proved, against the claimant or another involved party (e.g. the manufacturer of faulty equipment), it can have a dramatic effect on the final compensation amount awarded.

Illegal activity You may have heard stories about burglars being injured and attempting to sue the owners of a property for compensation. While this could hypothetically occur, a defence for this scenario would be that the claimant was injured whist committing a criminal act. A defence of 'illegality' can be used where a person was involved in criminal activity at the time of the accident, such as in cases of unlawfully trespassing. In situations such as these the defendant would not have a duty of care towards the claimant and a claim would most likely fail. Claim is out of time Someone making an injury claim has three years from the date of the accident or incident to start formal court proceedings (issue a claim with the court). This three-year time limit however is not always straightforward as it may also start from the date the person first had knowledge of the injury which may be several years after the incident that caused it, such as in industrial decease cases. In the case of children, the three-year limitation period doesn't start until they become an adult on their 18th birthday, so a child injured at age 10 will have until they are 21 to lodge a claim. These timeframes are dictated by the Limitation Act and if a claim is submitted outside the limitation period it can be very difficult for a claimant to show a valid reason why a claim wasn't submitted in the allowed timeframe. Therefore, often the claim may be dismissed regardless of the injury, circumstances or liability. Contesting a personal injury claim.

A poorly defended compensation claim can cost you or your business thousands and in extreme cases result in its closure. While rigorously defending a lost cause is not likely to be cost effective, a thorough and carefully constructed defence can mitigate the compensation you are exposed to.

If you are fortunate enough to have relevant home, employer's liability or public liability insurance in place, then your insurance company may provide a solicitor to fight the PI claim on your behalf. Therefore, when you speak to them it's important to have an idea of what facts you dispute and evidence you can provide to support your case. If you don't have valid insurance to cover a compensation claim, then it is critical to seek direct advice from defendant personal injury lawyers as soon as possible. Contesting a personal injury claim can be a complex task, but the sooner you seek advice the better your defence prospects will be.

Comments

When you are owed money, hindsight can be a wonderful thing.

All too often in the rush to complete a business transaction or lending money to a friend in need, you won't think to put in place a legally binding agreement that formalises the arrangement beforehand. After all, you have every intention of holding up your end of the deal and so assume the other party will too. But if payment doesn't happen and your previous agreement starts turning into a dispute over what is owed, you may need to consider what legal avenues are open to you to get your money back. The success of any legal action will then depend on what evidence you can provide to show that the debt is owed.

Can you take someone to court for owing you money?

Yes, but the 'burden of proof' will be on you as the Claimant to show that the amount you are claiming is due. Court should be your last resort in attempting to recover your money and so you should be confident that you have a strong case, sufficient evidence and follow the set pre-action procedure prior to issuing a claim (e.g. sending a letter before action, attempting negotiation etc.)

Ultimately the decision on who owes what will be down to a judge's ruling based on:

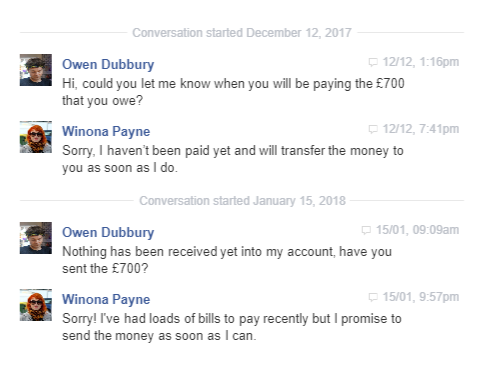

Owed money but no contract! SMS or messages on social media can help prove a debt is owed. SMS or messages on social media can help prove a debt is owed.

In the absence of a written contract or agreement being in place, there are various other pieces of information that you may be able to secure which can provide evidence that the money is due.

Bounced cheque or returned direct debit While the use of cheques is diminishing, hundreds of millions of cheques are still issued every year. If your debtor has sent you a cheque that bounced or agreed to a direct debit that has been returned, it is often all the evidence that you need to prove a debt is owed. In law a cheque is considered a 'promise to pay' and so can be used as a clear admission that money is due. Unpaid invoices It is not uncommon for a business to invoice without a contract. Most businesses use invoices to request payment so providing copies and proof of them being issued to a customer or supplier will go a long way in proving that a debt is owed, even if they aren't directly attached to Terms of Business or a contract. Furthermore, if you provided regular statements of the amounts owed and showing overdue, then these will also be useful as evidence. Evidence of chasing debts Once a payment is overdue you will have hopefully contacted the person or company to chase the debt. Emails, letters, texts or messages exchanged on social media (Facebook, Twitter etc.) can all be used to help prove a debt is owed and overdue. If the other party has responded to you apologising or asking for more time, then this admission will be extremely valuable in proving that they don't dispute that they actually owe the debt. So, it's important that you save or screenshot these messages in the event they are needed. Loaned money without a contract Without an I.O.U. or a loan agreement in place, proving that money provided to someone was a loan that needs to be repaid can be difficult. This is because often money given to friends, an ex, or family member is considered a gift and so isn't required to be paid back. Enforcing a verbal agreement that money is owed will hinge around providing evidence to show that the cash was transferred as a loan along with any repayments e.g.

Witnesses to the arrangement When little or no documentation exists to prove a debt, having an independent witness to a verbal contract can be invaluable. For example - with a business transaction, did an employee take the order over the phone, deliver goods or perform a service where payment was verbally agreed with the customer? If money was lent to a friend, was another person present to witness the agreement of how/when they were going to pay you back? But even if an independent witness isn't available, you as a claimant can also present your version of events to the court in a written witness statement. Any witnesses may then need to attend court should the claim go all the way to a hearing. Debt disputes with no contract.

Without a written agreement, there should still be plenty of information that you can pull together to prove what you are owed. However, if the other party disputes the amount, or that any debt is owed at all, then you may have a fight on your hands that needs to be settled in court.

It will then be down to the evidence you can gather and how your claim is pleaded to convince a judge that you are entitled to the money owed in the absence of a legally binding written contract. So, obtaining legal advice on the evidence needed for a debt recovery claim and your prospects should be your starting point.

When a friend asks to borrow money it can be difficult to refuse. We don't think twice about saying no or hanging up to telemarketers that want us to part with our money, however when it's someone familiar that is asking, your usual good judgement can quickly disappear.

But if after you have given the loan, your trusted friend disappears just as quickly, then you've now got a dilemma. This scenario is unfortunately all too common, with payment service Paym finding that over 12 million people in the UK admit to having fallen out with friends or family over money. Just under a third of these instances were from lending money to friends of only up to £100. But after repeatedly asking your friend for the money back, being reasonable and understanding of their circumstances but ultimately being left out of pocket, how can you get money back from someone who borrowed it? Can you actually take your friend to court? How can you prove you are owed the money?

Before involving the court you need to think about your prospects of success. You'll need to have some kind of evidence that you lent the money in the first place and that your friend hasn't paid you back.

If you've got a signed contract, loan agreement or IOU then that's ideal, but the evidence of the loan doesn't always necessarily have to be written. A legal contract can be verbal if it was just an arrangement you discussed and agreed between yourselves, however there still needs to be something that a court can see, like:

Does your friend actually have the money to repay you?

You can't get blood from a stone, so if your friend has no cash or assets then there may be little gained from taking them to court. It will cost you money to issue the claim and you'll rack up further fees to enforce any judgment from the court (bailiffs etc.) to perhaps end up with nothing or very little.

But if your friend is employed, owns a car, has equity in a house or some other assets that would cover the debt then it's reasonable to assume that you can make a recovery from them by going through the courts and obtaining a County Court Judgment (CCJ) against them.

How to get money back from a friend."Nearly 2 out of 5 people admit they don't always pay friends back, and one in ten say they have avoided paying money back to family on purpose." - Research by Paym  Not getting paid back can be frustrating Not getting paid back can be frustrating

If you've secured evidence of you making the loan and believe your friend has the means to pay you back, then it's time to start getting serious. Sometimes the realisation that you're willing to take the matter further can snap your friend into action.

First step is to write a simple (but formal) 'Letter Before Action' which gives your friend a final chance to settle the debt before court proceedings are started. As a minimum your letter should include:

Keep a copy for yourself and send the letter in the post to their home address, or where they are currently living. The best outcome is that your friend pays you back or at the very least you agree a payment plan that starts to recoup the loan. That way you avoid court costs and will eventually get your money back. If your friend subsequently fails to comply with the payment plan then at least you'll have further evidence to help with court proceedings. Also if you want to add additional weight to your claim, you can get a solicitor to draft and send the debt letter which should only cost around £50.00. Taking friends or family to the Small Claims Court.

The last resort in recovering your money is to take your friend to court. This is normally done through the small claims court (for amounts up to £10,000) and will involve you completing some paperwork, submitting it to the court and paying a court fee.

Instructions on how to make a claim can be found on the Gov.uk website. Straightforward claims are able to be done on your own with a little time and effort, but can get complicated if the claim is defended, interest is able to be added or bailiffs need to be instructed etc. As such depending on the amount, it may be wise to instruct a solicitor to handle the claim who should be able to do this for a fixed fee plus disbursements (the court fees). Some of your legal costs can also be recovered from the debtor as part of your claim. Remember getting money back from a friend, an ex-partner or family member can be complex and emotional process, so having your lawyer deal with the proceedings and ongoing contact with the debtor may help in the long run. "Before borrowing money from a friend, decide which you need most"

Being owed money by a trusted friend who won't pay you back is never a good situation to be in, and how you proceed will likely be determined by how much you want to maintain the friendship.

If your friend is in real financial difficulty then piling on court proceedings may not help them or their family, so you may want to consider the full impact of taking matters further. But this is a judgement and a financial call that only you can make. It is also worth noting that you generally have six years to start legal proceedings to recover a debt. You should never feel guilty about pursuing money owed to you which you lent in good faith. Remember if anyone has jeopardised your friendship it's a friend who has decided to stop paying and communicating with you. |

About UsCatalyst Law are team of legal professionals with over 20 years' experience helping businesses and people with their legal problems. Categories

All

Follow us on:Archives

March 2024

|

RSS Feed

RSS Feed